For every $100,000 of costs shifted from 39-year property to 5-year property, the net present value of the tax benefit is about $16,000 (assuming a 35% tax rate and 5% return on investment).

What is Cost Segregation?

Cost segregation is an IRS-approved strategic tax savings tool that allows companies and individuals, who have constructed, purchased, expanded, or remodeled any kind of real estate to increase cash flow by accelerating depreciation deductions and deferring federal and state income taxes owed through segregating (reclassifying) non-structural building components (5-, 7- and 15-year IRC Section 1245 Tangible Personal Property) and structural building components (27.5- and 39-year IRC Section 1250 Depreciable Real Property). The primary goal of a Cost Segregation Study is to identify all construction-related costs that can be depreciated over 5, 7 and 15 years. For example, 20% to 50% of the total electrical costs in most buildings can qualify as personal property (depreciated over 5 or 7 years).

Reducing tax lives results in accelerated depreciation deductions, a reduced tax liability, and increased cash flow. Building owners often use this tax savings to reinvest in their businesses, purchase more property, apply to their principle payment or spend on themselves.

What are the benefits of a Cost Segregation Study?

- Generates immediate increase in cash flow through accelerated depreciation deductions.

- Reduces income taxes and can also reduce real estate property taxes.

- Provides an easy opportunity to claim ‘catch up’ depreciation on previously misclassified assets.

- Provides an independent third-party analysis that will withstand IRS review.

When should a Cost Segregation Study be conducted?

The ideal time for a Cost Segregation Study can vary depending on a client’s tax situation. A free preliminary analysis can help determine the right timing and strategy.

- Post-purchase, Remodel, or Construction: “Look-back” Cost Segregation Study: A Cost Segregation Study can be completed anytime after the purchase, remodel, or construction of a property. In fact, current Internal Revenue Service procedures make it easy to go back and claim missed depreciation on assets acquired as far back as 1987 without amending prior tax returns.

- Year Placed in Service: The optimum time for a Cost Segregation Study for new owners, is during the year a building is constructed, purchased, or remodeled. This allows an owner to immediately optimize tax savings and accurately classify assets before the building even begins to depreciate.

- Pre-construction: For investors who are in the planning phases of construction or remodeling, the best time to consider a Cost Segregation Study is before the infrastructure of the building is set.

What kind of real estate qualifies?

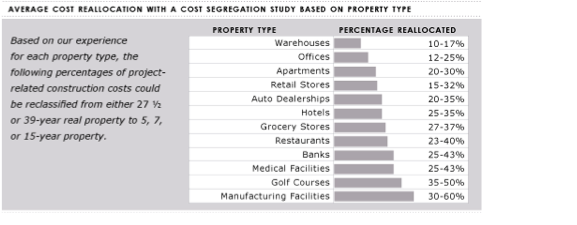

Any structure used for business or as rental property, is eligible for the benefits of Cost Segregation. The graph below represents the percentages of project-related construction costs that could be reclassified from either 27 ½ or 39-year real property to 5, 7, or 15-year property.

Projects benefiting from Cost Segregation include shopping malls, airports, sports facilities, driving ranges, resorts, health care facilities, industrial buildings, auto service centers and more.

Any leasehold improvements can also qualify for a Cost Segregation Study. These interior build- outs generally produce a proportionally higher ratio of qualifying property. Therefore a Cost Segregation Study that analyzes the costs of leasehold improvements can be even more beneficial.

What is involved in the study?

A quality Cost Segregation Study evaluates all information including available records, inspections, and interviews, and presents the findings in a clear, well-documented format. Our process for conducting a detailed Cost Segregation Study includes:

- A review of all cost detail for the property including but not limited to: the general contractor’s application for payment, construction invoices, change orders, depreciation schedules, and appraisals.

- An inspection of the facility to fully understand its use and condition, as well as to gather information that further supports the classification of capitalized costs into their appropriate class lives.

- Photographs are taken of qualifying construction components and included in our report.

- A review of all blueprints (if available) and the performance of quantity take-offs and cost estimates for personal property not segregated in other cost information.

- A reconciliation of all construction costs and estimates of the actual amounts incurred by tax life. This step includes adjusting estimates to account for location, time, and physical condition. We also perform an allocation of soft costs to any direct cost in each category to maximize your total benefits.

- Preparation of a report: Our report complies with the IRS standards stipulated in the Audit Techniques Guide for Cost Segregation Studies.